A healthcare proxy, or medical power of attorney, designates someone you trust to make medical decisions if you're unable. This crucial document prevents family conflicts and ensures your wishes are honored. Legacy Planning Law Group can help secure your healthcare preferences today.

Different Types of Power of Attorney (and Who Needs Them)

By Jessica Sillers — Mar 19, 2019

The plan is for us to have minds like a razor for the rest of our lives. That said, protecting our family sometimes means hoping for the best while planning for the worst.

That’s where power of attorney can be helpful, in addition to other estate planning such as a last will and testament.

Power of attorney documents let someone make legal and financial decisions for you if you can’t. We’ve done the research to help you understand the different kinds of power of attorney, and which may make sense for your situation.

You might choose to put a power of attorney in place for yourself, just in case. Additionally, if you have aging parents or other relatives, you might encourage them to set up power of attorney while they’re still able.

And yes, married couples often need POA, too, even if they have joint accounts! We’ll break down your questions, from “what is POA?” to “who can override a power of attorney?” and “how do I get a power of attorney?”

What Is Power of Attorney?

People ask us a lot for the definition of a POA: A power of attorney document names someone (called the “agent”) to make legal decisions on another person’s behalf (the “principal”) if the person is not able to. For example, if you got into an accident that left you in a coma, or if you suffered from dementia, this would enable someone else to step in and manage your affairs and your property.

The catch is, the document needs to be in place before you’re declared legally incompetent to make decisions for yourself.

You can name multiple agents on a POA document. Often, this means a top choice and a few alternates, although you can specify multiple people who have to work together as co-agents (such as multiple adult children).

If you’re interested in naming co-agents (or if you’re named along with someone else on a relative’s POA), make sure the document answers these questions:

-

Can co-agents act independently, or do all of them need to agree on every decision?

-

What happens if a co-agent isn’t responding promptly regarding a certain decision or document?

-

Is there language in the POA to settle disputes between agents? What happens if co-agents can’t resolve a dispute?

Generally speaking, you can get a power of attorney by having a lawyer draft these documents for you. POA documents can take multiple forms. Let’s jump into the main types you should know about.

Different Types of Power of Attorney

There are a number of different types of POA, which vary according to how much control they grant the agent. They can also differ by how long they last and when they take effect.

Durable Power of Attorney

“Durable” is an umbrella term that applies to most POA documents. These are typically used in cases where you are concerned about becoming incapacitated in the future. With durable power of attorney, the agent’s power continues indefinitely after the point when you’re legally not able to make your own decisions.

Depending on your state’s laws, you may not need to inform your agent that they’re named in your durable power of attorney at all. (Though it’s still a good idea!) It’s also important to note that you’re not giving up control over your finances before you’re incapacitated. The agent has legal access as soon as the POA takes effect, but you can revoke their power at any time or for any reason. And in the meantime, you won’t lose any of your own access or control over your accounts.

Your agent has a fiduciary duty to act in your best interests, not theirs. Your bank account isn’t their ATM by virtue of having access. If a bank suspects an agent of abusing their power, or if the durable power of attorney is “stale” (i.e. hasn’t been re-signed in the last few years), the bank can turn an agent away.

You (or someone who’s concerned about your financial welfare) can also take your POA agent to court or contact state adult protective services if they suspect that the agent is misusing your funds. A court can make the agent return misused money or other assets, and depending on the misuse, there may even be grounds for criminal prosecution.

Non-Durable Power of Attorney

A non-durable power of attorney document, on the other hand, isn’t a “forever” thing, and it’s not intended for cases of incapacitation. In fact, it isn’t actually valid if you’re legally incompetent.

Rather, a non-durable POA is used when you need someone to act on your behalf for a specific event when you can’t be present yourself. If you’re taking a job across the country, for example, an agent named under non-durable POA can sign documents to get you an apartment in the new city.

Non-durable POA takes effect as soon as all documents are signed, and ends when:

-

The specific transaction you outlined in the non-durable power of attorney document is complete, or the expiration date named in the document passes

-

You revoke the document for any reason

-

You’re legally incapacitated

The reason a non-durable POA ends if you’re incapacitated is that this document is almost always meant to accomplish a very specific objective (like signing a legal agreement for you when you can’t be there in person).

If you get in a car crash and end up in a coma, whatever plans you had—such as purchasing real estate or selling your business—may not be wise in light of this new emergency. Think of it as the financial version of lending a neighbor a house key while you’re on vacation: You’re OK with them accessing your place to water plants or feed the cat. But if anything happened to you, you might not want that permission to continue.

Therefore, it’s actually a sort of security feature for you that a non-durable POA expires if you become incapacitated. That way, someone who was authorized to do one thing doesn’t end up with indefinite access to your account.

Immediate POA

An immediate power of attorney document takes effect as soon as it’s signed. That said, most people don’t expect to use it until they’re legally incompetent, such as after a stroke that impairs cognitive ability.

Depending on your state, the agent may or may not need to sign the document. You also need to renew your POA according to state guidelines by re-signing the document (every one to three years is pretty common).

“The agent you name under the POA isn’t supposed to go out and start using it unless and until the principal becomes disabled,” says Evan H. Farr, certified elder law attorney. “The reality is, if you give someone immediate POA and they go off and start doing stuff, you’re going to find out right away.”

An agent also has to act in your best interest. This person can’t “decide” that what you really wanted was to fund their round-the-world luxury tour instead of paying for long-term care for you, for example.

General Power of Attorney vs. Limited Power of Attorney

You can write a POA in two forms: general or limited.

-

A general power of attorney allows the agent to make a wide range of decisions. This is your best option if you want to maximize the person’s freedom to handle your assets and manage your care.

-

A limited power of attorney restricts the agent’s power to particular assets. For example, you might grant someone access to a bank account, but not your house or investment portfolio.

In either case, this is a highly technical legal document. DIY options exist online, but your best bet is to work with an experienced elder care law attorney or another attorney specializing in estate planning. That holds true whether you’re looking for a general power of attorney or a limited power of attorney.

Springing Power of Attorney

Springing power of attorney is similar to immediate POA in that it works when you’re incapacitated. The difference is that it only “springs” into effect once you meet conditions you set to declare you legally incompetent.

“Most estate planning attorneys don’t use springing POAs because they create more problems than they’re designed to solve,” says Farr. For example, let’s say that you define the “springing” condition as your being deemed incompetent by two physicians. In a case like that, the document is useless if for whatever reason you refuse to show up for a doctor’s visit.

Some health conditions, including dementia, involve good days and bad days. That can make it harder for doctors to make a definitive call on a person’s cognitive ability (and therefore harder to definitively “spring” the POA into action). If the springing conditions are too vague, a court might need to get involved to rule on the principal’s status.

Remember, you should choose someone you trust to act as your agent. If you’re considering a springing power of attorney because you don’t want to give this person power until it’s urgent, your hesitation could be a sign. Do you not fully trust this person? If so, you might consider naming someone else.

The Rights That Do (and Don’t) Come With Giving Someone POA

Again, having legal access to your account doesn’t mean your POA agent has more power than you, or that they can do anything they want with your money. POA power isn’t like being co-owner of a joint account, for example. If you and an agent disagree over a financial decision, your decision governs (although, to be fair, if they have already made a POA-authorized purchase, you may need to go through some hurdles to get that money back).

Your agent can’t swoop in and take over simply because you’re making decisions they disagree with, and you can revoke their power in writing anytime you want.

Forgetting you’ve named someone as your agent may not be as serious of a risk as it sounds, because financial institutions often take a conservative approach to working with an agent.

An outdated POA, or a major event like divorce (if your spouse was your agent), is often a red flag for a bank. If the financial institution suspects that something’s amiss, they can and often will refuse to honor the POA. It’s often recommended that you review any POAs on the timeline your attorney suggests, so you can make updates.

Working with an attorney who has plenty of experience writing POA documents is also a major part of setting up the right balance of restrictions and access for your agent. These documents are understandably complicated, and having a clearly articulated plan goes a long way toward outlining the kinds of decisions you want your agent making on your behalf.

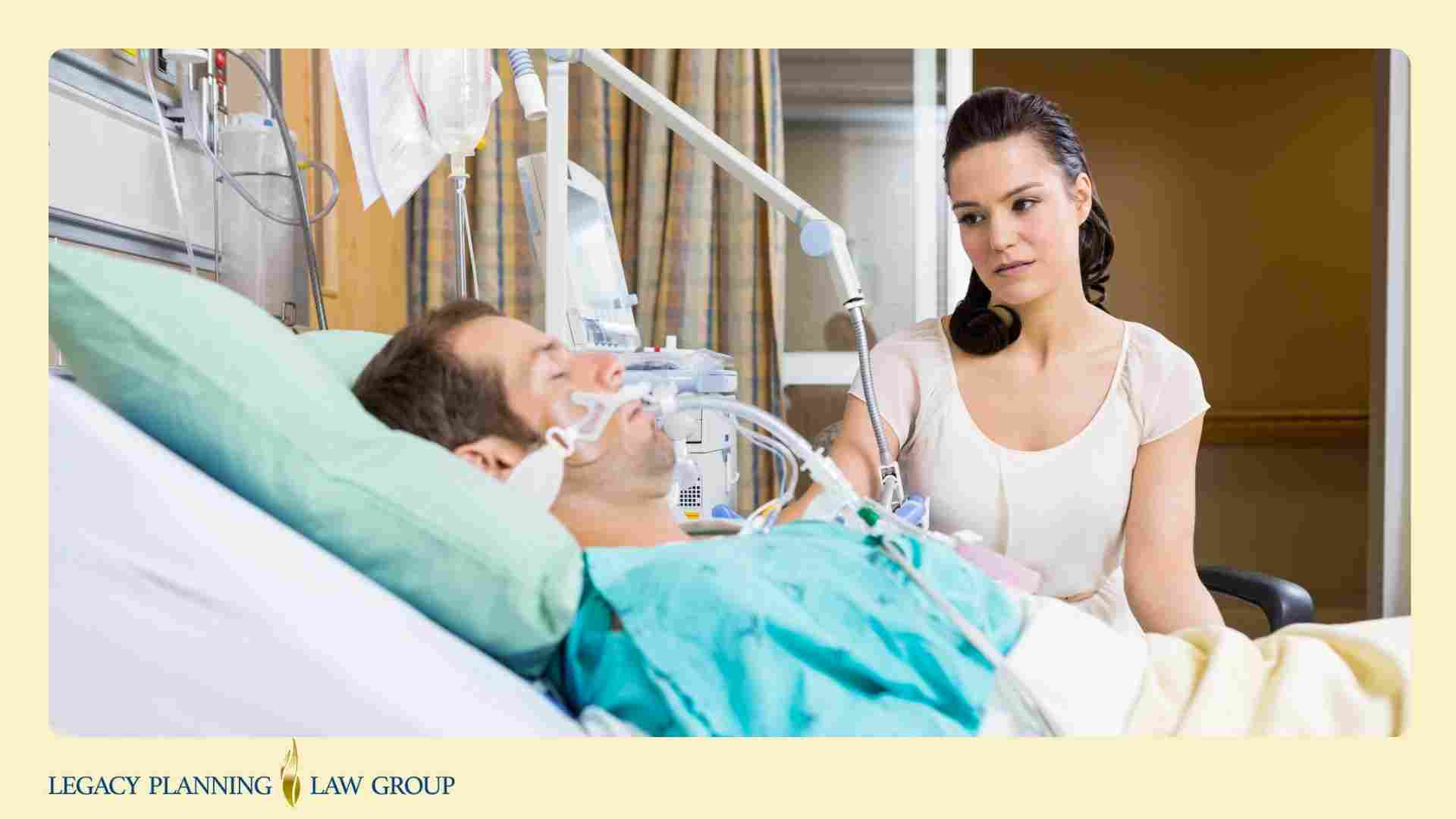

Beyond the Money: Medical Power of Attorney

Consider writing separate POA documents for your health and your finances.

“There’s no benefit to combining them,” says Farr. “The banks don’t need to see your healthcare wishes, and the hospital doesn’t need to see your financial wishes. Even if you have the same person as your agent, you may choose different alternates” for your medical power of attorney and your financial one.

Medical POA is part of a larger document called an advance medical directive, which includes three main components:

-

Medical POA: Who will make decisions on your behalf?

-

Near-death directive: What are your wishes for care (or when to stop treatment) in case of severe illness or coma?

-

After-death directive: What you want done with your body (organ donation, cremation vs. burial and so on)?

Who Needs Power of Attorney

Just about anyone with financial assets should consider a POA. The possible exception might be single people who don’t own a home and don’t support anyone financially. But even then, having a POA could enable someone you trust to dictate the use of your funds to manage your care if something happened to you.

If you’re married and share joint financial accounts with a spouse, you still need to draw up a POA document. In fact, it can be even more critical.

“Most financial institutions won’t allow one of the owners to simply take out all the money or close account. They want both people or someone who has POA,” says Farr. “With real estate, you always have to have both people involved. Even if they had no bank account and their only asset was the house, you need POA.”

If you’re in a coma, or you have a stroke that leaves you mentally unable to make legal decisions, your spouse may decide it’s best to downsize to a smaller house, for example. Without POA, they can’t simply do it.

Instead, they’d have to go through what Farr calls, “The lovely and wonderful nightmare of living probate—lovely and wonderful for the attorneys who make tons of money on it, and a nightmare for the people involved.”

Your spouse, parents or whoever will handle legal and financial matters would have to go to court to petition for you to be declared legally incompetent. Once that happens, the court would name a guardian (responsible for your personal and health-related care) and a conservator (responsible for your finances). These can be the same person, and the terms used to describe this role vary by state.

From there, the conservator has to file annual accountings of the money coming in and out of your accounts. These need to be accurate to the cent, or the probate court may not accept the records. At that point, even more legal proceedings could come into play.

Figuring out POA spares your loved ones from going through a time-consuming, labor-intensive legal process at a time when they already have a lot to worry about.

Questions POA Agents Should Ask

If a family member names you as his or her POA agent, here are some things you’ll want to discuss beforehand:

-

What aspects of your finances am I responsible for?

-

Do you have other legal documents in place, like a will, trust and a medical POA?

-

Am I also being named as successor trustee (the person who takes control of a trust fund after the initial trustee dies) on any trusts you’re setting up?

-

If I’m managing finances for your long-term care, which options have you looked into? What kind of care do you prefer, such as transitioning to a nursing home versus hiring an aide for in-home care? How long will this account be able to fund it?

-

Are you planning to manage your finances independently until you legally can’t, or do you want me to take on any responsibilities before then?

It’s important to note again that you might not know if you’ve been named the agent! A good first step if you know your relatives are doing estate planning is to check whether you’re named on any documents.

Power of attorney enables your loved ones to handle critical financial matters for you if you can’t. It can even protect your spouse from being financially trapped if something happens to you.

You’d probably want someone you trust to handle medical decisions for you if you couldn’t speak for yourself. Similarly, it’s a good idea to consider who will keep the money side of your life from crashing in an emergency.

Power of attorney can make it easier for a loved one to pay your bills, keep you out of debt and make sure your dependents are provided for.

Read more related articles here:

Consumer Pamphlet: Florida Power of Attorney

Also, read one of our previous Blogs at:

What are the Different Kinds of Powers of Attorney?

Click here to check out our On Demand Video about Estate Planning.

Related Posts